Resilience is the new black.

In the fashion industry Black is always in style; saying something is ‘the new black’ means that it is the hottest new thing. This saying isn't just limited to fashion; the phrase in the black also refers to business' profitability.

So what do I mean resilience is the new black? As I watch the world burn down and see the collapse of the economy and environment into a single distinction, (they reliant on each other) I've been spending a lot of time thinking about what a new financial system would look like. I assert that because the economy is reliant on the environment, that financial instruments and capital allocation will be connected to data and global policies that measure the actions of people and organisations to cool the planet.

As we realise its time for a change, our economy will begin to value investment in regenerative and restorative practices. When you consider all products and services will be measured for their environmental footprint, and the actual cost of creating economic value; restorative and regenerative ways which develop communities and build connections with their customers will be more profitable.

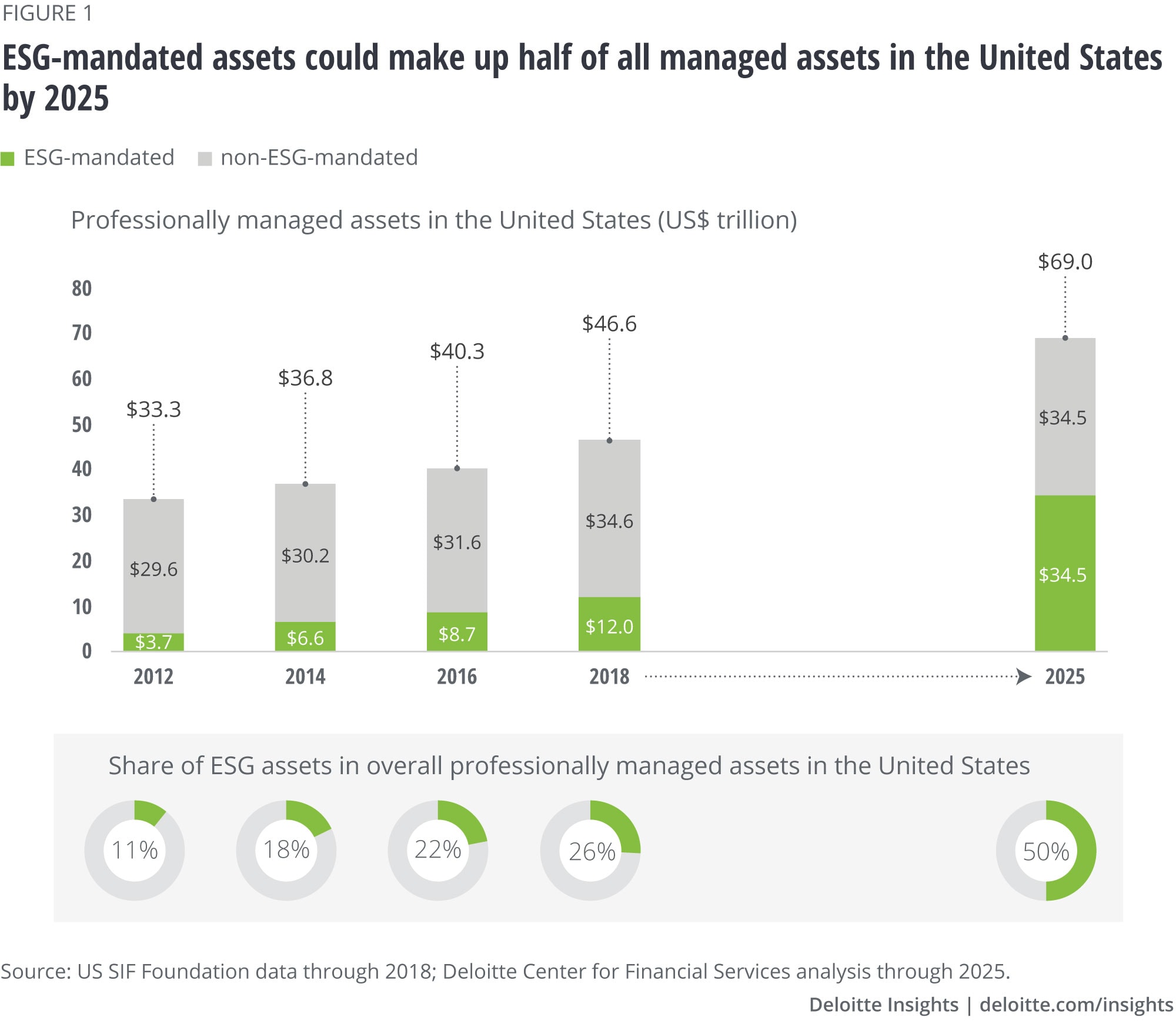

I'm not talking about a carbon credit or greenwashing; I'm talking about a financial product that is a smart contract linked to data that measures progress against a sustainability goal. In this class of financial asset the finance will not be separate from the monitoring or the metrics; the capital won't be allocated solely on the ability to repay the capital is it is now, it will be measured on regenerative practices. Retail investors are already looking into invest in social impact and global funds are being directed to invest in ESG. The question is how is this transparent and measured.

The risk of environmental disasters can't simply be insured. We need to see systemic change in human behaviour, and capital markets are efficient at allocating resources for the best return with the lowest risk.

The problem is as our financial services industry has moved us towards an insurance model. Our historical risk models are based on actuarial data that dates back to the time of the knights of the round table (mid 12th century) and they didn't need to consider climate change. As there are only three ways to mitigate risk; remediate it, accept it (ignore it) or transfer it, we need to accept the fact that we can’t transfer climate liability via insurance, or just ignore it so we need new models to remediate it.

Resilient businesses will begin to attract premium capital because sustainability isn't going to cut it any more, we can’t maintain the status quo, We need to turn the clock back; this will drive regenerative business practices which introduce planetary resilience.

The planetary boundaries concept presents a set of nine planetary boundaries within which humanity can continue to develop and thrive for generations to come.

Source: https://www.stockholmresilience.org/research/planetary-boundaries.html

Businesses that have regenerative practices will be lower risk, organics, circular economy, carbon-neutral, it's not like we don't know what we need to do. We need to move to regenerative business models at a speed that we never have previously to avoid crossing planetary boundary guidelines.

The issue is our capital markets are not efficiently allocating capital to lower risk assets that take into consideration the impact on all conditions of life, i.e. the human and environmental cost of polluting or non-transparent (ethical) supply chain practices.

So how do we introduce transparency at scale? In five years, blockchain or some other decentralised technology like Holochain will be mature, and IoT (Internet of Things) will be pretty much everywhere and in every device.

We'll have the ability to create contracts using code not Microsoft Word, and the IoT platforms will link data back to the financial service. This is where we can start to create new asset classes; but the key is, how do we measure the right things?

Metrics can tell one part of the story; for example, has there been an improvement in the environment or supply chain practices over time. This will be one indicator, but what we're looking for is a change in behaviour. The financial product can't only link to the data metrics; it has to connect to the actions that have been taken to reach the goal.

Think about it like this, how many times did you set an aim you didn't reach, but you took the actions to achieve that aim and reached a different outcome you couldn’t see when you started. If we measure the wrong thing, we'll penalise the borrower of capital. Also, we are only an element of the environment; we can't control everything in that environment, relying solely on data generated by devices removes the human element when this is the crucial aspect of financial service that considers resilience.

We can already see corporations using IoT data for measuring supply chain risk in global shipping or from local car insurance providers who measure speeding.

The questions I have on my mind is how are we creating a global infrastructure which breaks down the inefficiencies that have caused our organisations to put profit over people, profit over sustainability and consume more resources than they create due to waste and pollution.

We have the choice to learn from our mistakes, but I don't think the future of the financial services industry is going to be created by the current stakeholders. The incumbent solutions are centralised and monopolistic and slow, and the last time I looked, global movements don't start from corporations, they start from communities.

Resilient systems are lower risk, more productive, I know it. I've been on organic farms and seen the output; I've seen how this impacts the soil, and what flow impact that has into the nutrient density.

As the convergence of technologies occurs and the capital markets prioritise risk, you can be sure that they will take into consideration the environment and people they impact. Financial products in the future will be smart, as they will real-time link data to regenerative outcomes. This will favour resilient companies because they prioritise the environment and human rights at their core, and this will lower their risk of business disruption which lower the risk of non-payment, thus lowering the relative cost fo capital.

We need to creating open standards to unlock capital focused on resilience. How do we build a four horizon model that shifts the entire industry to financial services model that put environmental risk and human rights at the forefront of all capital allocation because that creates resilience…. and more importantly can we do it fast enough to keep within the planetary boundary guidelines?